Introduction

Most taxpayers in India focus almost entirely on deductions under Section 80C or Section 80D. They invest in ELSS funds, buy life insurance, and pay health insurance premiums to reduce their taxable income. While these strategies help, they often overlook a more powerful opportunity within the Income Tax Act, 1961 – certain types of income are completely tax-free and do not form part of your taxable income at all.

This guide explains all major legal sources of tax-free income in India, the conditions attached to each, and how they can be combined for efficient tax planning.

What Is Tax-Free Income Under Indian Tax Law?

Tax-free income refers to income that is excluded from your total taxable income under the Income Tax Act, 1961. These incomes are primarily covered under Section 10 and other provisions, and most of them come with specific eligibility conditions.

Tax-Free vs Tax-Exempt vs Deductions

| Concept | What It Means | Example |

|---|---|---|

| Tax-Free Income | Income excluded from taxable income (subject to conditions) | Agricultural income |

| Tax-Exempt Income | Income exempt up to limits or conditions | Gratuity up to ₹20 lakh |

| Tax Deduction | Amount reduced from taxable income | Section 80C |

Example: Mr. Ram earns ₹8 lakh from salary and ₹5 lakh from agricultural activities. Only ₹8 lakh is taxable. Agricultural income is exempt, though it may be considered for rate calculation in certain cases.

9 Legal Tax-Free Income Sources in India

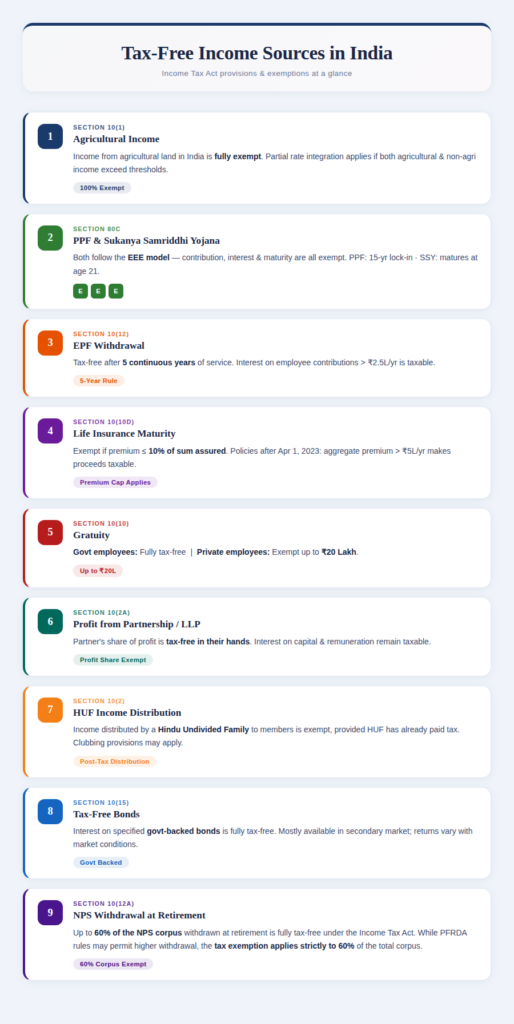

1. Agricultural Income (Section 10(1))

Agricultural income from land situated in India is fully exempt from income tax. If agricultural income exceeds ₹5,000 and non-agricultural income exceeds the basic exemption limit, partial integration is used to determine the applicable tax rate.

Example: A person earning ₹6 lakh from agriculture and ₹8 lakh from business will pay tax only on business income, but the applicable tax rate may be influenced by the agricultural income.

2. Public Provident Fund (PPF) and Sukanya Samriddhi Yojana (SSY)

Both schemes follow the EEE (Exempt–Exempt–Exempt) model:

- Contributions qualify for deduction under Section 80C (old regime)

- Interest earned is tax-free

- Maturity proceeds are fully tax-free

PPF has a 15-year lock-in, while SSY matures when the girl child turns 21.

3. EPF Withdrawal (Section 10(12))

EPF withdrawals are tax-free if made after completing five continuous years of service. If withdrawn earlier, the amount becomes taxable. Interest on employee contributions exceeding ₹2.5 lakh per year (₹5 lakh where there is no employer contribution) is taxable.

4. Life Insurance Maturity (Section 10(10D))

Maturity proceeds are tax-free if the annual premium does not exceed 10% of the sum assured. For policies issued on or after April 1, 2023, if the aggregate premium exceeds ₹5 lakh in a year, the maturity proceeds become taxable.

5. Gratuity (Section 10(10))

- Government employees: fully tax-free

- Private employees: exempt up to ₹20 lakh

6. Share of Profit from Partnership Firm or LLP (Section 10(2A))

The share of profit received from a partnership firm or LLP is tax-free in the partner’s hands. Interest on capital and remuneration received by the partner are taxable.

7. HUF Income Distribution (Section 10(2))

Income distributed by a Hindu Undivided Family (HUF) to its members is tax-free in their hands, provided the HUF has already paid tax. Proper structuring is important, as clubbing provisions may apply in certain cases.

8. Tax-Free Bonds (Section 10(15))

Interest earned from specified government-backed bonds is tax-free. Most of these bonds are now available only in the secondary market, and returns may vary based on market conditions.

9. NPS Withdrawal (Section 10(12A))

Up to 60% of the total corpus withdrawn at retirement is tax-free. While regulatory rules may allow higher withdrawal, tax exemption under the Income Tax Act clearly applies only to 60% of the corpus.

Quick Reference: Tax-Free Income Sources

| Section | Income Type | Key Condition | Limit |

|---|---|---|---|

| 10(1) | Agricultural income | Land in India | No limit |

| 10(11/11A) | PPF/SSY | Lock-in applies | No tax on maturity |

| 10(12) | EPF | 5 years service | No limit |

| 10(10D) | Insurance maturity | Premium conditions | Policy-specific |

| 10(10) | Gratuity | Employment type | ₹20 lakh |

| 10(2A) | Firm profit | Firm taxed | No limit |

| 10(2) | HUF distribution | Proper structure | No limit |

| 10(15) | Tax-free bonds | Govt specified | Depends |

| 10(12A) | NPS | Retirement | 60% corpus |

Tax-Free Income vs Tax-Saving Deductions

| Feature | Tax-Free Income | Tax Deduction | Capital Gains Exemption |

|---|---|---|---|

| Tax Treatment | Not included in income | Reduces taxable income | Specific exemption |

| Example | Agricultural income | Section 80C | Section 54 |

| Applicable Regime | Both regimes | Mostly old regime | Both regimes |

Smart Tax Planning Strategies

1. For Salaried Individuals

Maintain taxable income within ₹12 lakh where possible and combine EPF, PPF, and employer NPS contributions to build a tax-efficient portfolio.

2. For Business Owners

Use partnership structures, HUF planning, and tax-free investments to optimize income distribution.

3. For Retirees

Combine gratuity, EPF withdrawals, leave encashment, and NPS benefits to receive a large portion of retirement income tax-free.

Stacking Strategy Example

| Income Component | Amount |

|---|---|

| Salary | ₹12,00,000 |

| Standard Deduction | -₹75,000 |

| Taxable Income | ₹11,25,000 |

| Tax-Free Income | Additional |

Final income tax payable: Zero (subject to conditions and exclusions)

Conclusion

Tax-free income is one of the most effective yet underutilized tools in Indian tax planning. Instead of relying only on deductions, structuring income through exempt sources can significantly reduce your tax burden.

With proper planning and compliance, it is possible to legally minimize or even eliminate your income tax liability.

FAQs

No, it is fully exempt, but may be used for rate calculation in certain cases.

Unlimited if received from relatives; otherwise taxable above ₹50,000.

No, it is fully tax-free.

Tax-free after 5 years; otherwise taxable.

Effectively yes under the new regime due to rebate, but not for special rate income.

Yes for government employees; up to ₹20 lakh for private employees.

Up to ₹25 lakh for private employees at retirement.

Tax-free if conditions are met; taxable if premium exceeds ₹5 lakh (post-2023 policies).