Here is something that happens more often than you would think: a business owner files GSTR-3B diligently every month, assumes they are fully compliant, and then receives a notice because GSTR-1 was never filed, or was filed with errors. Their buyer’s Input Tax Credit got blocked. There is now a dispute, and suddenly, there is an urgent call to the Chartered Accountant to fix the issue.

GSTR-1 and GSTR-3B are the two most important GST returns for any regular taxpayer. They are filed separately, serve fundamentally different purposes, and both are non-negotiable.

If you have ever wondered why two returns are needed for the same period – or what exactly goes into each – this guide will answer every question a rational business owner should be asking.

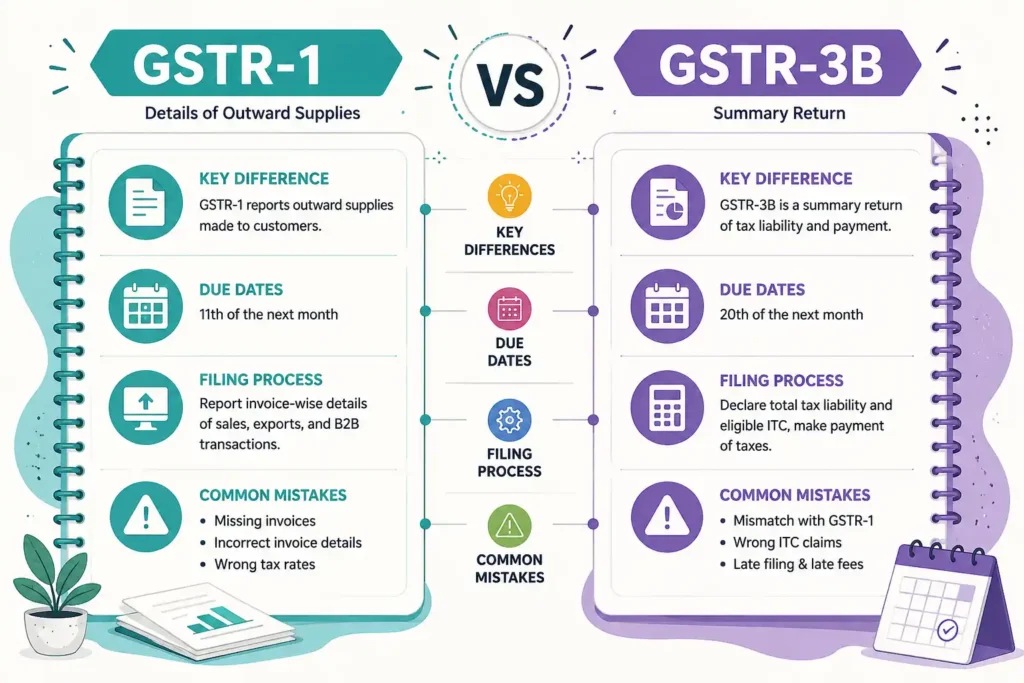

What is GSTR-1?

GSTR-1 is your outward supply statement – a detailed, invoice-level record of everything you sold during the period. Every B2B invoice, B2C transaction, export, credit note, debit note, and advance receipt must be reported here with full particulars.

Think of GSTR-1 as your sales register shared directly with the tax department. But it serves a second, equally important purpose – it determines your buyers’ ability to claim Input Tax Credit (ITC). When you upload an invoice in your GSTR-1, it automatically appears in your buyer’s GSTR-2B, which is the auto-generated purchase register. That is how they claim the GST credit on what they purchased from you.

| If you do not file GSTR-1, or file it with errors, your buyer cannot claim the GST credit they are legally entitled to. That is a direct financial loss for them – and it will cost you the business relationship. |

What Details are Included in GSTR-1?

- B2B invoices: all sales to GST-registered businesses, reported invoice by invoice

- B2C large invoices: inter-state sales above ₹2.5 lakh reported individually

- B2C small sales: intra-state and small inter-state B2C transactions reported as aggregate

- Export invoices: with or without payment of IGST

- Credit notes and debit notes: amendments or corrections to earlier invoices

- Advances received against future supply

- HSN / SAC-wise summary of all supplies

Who Needs to File GSTR-1 and When?

Every regular GST-registered taxpayer must file GSTR-1. Filing frequency is determined by annual turnover:

- Monthly filers (turnover exceeding ₹5 crore): Due on the 11th of the following month

- Quarterly filers under the QRMP scheme (turnover up to ₹5 crore): Due on the 13th of the month after the quarter ends

Even with zero sales during the period, a nil GSTR-1 must be filed. The portal will not permit subsequent returns to be filed if a prior GSTR-1 is pending.

What is GSTR-3B?

GSTR-3B is your monthly (or quarterly) summary return – and crucially, it is where GST is actually paid. While GSTR-1 captures the details of every invoice, GSTR-3B captures the aggregate tax position and settles the liability.

You declare your total outward supplies, the ITC you are claiming, any ITC reversals, and the net tax payable. When GSTR-3B is filed, the tax due is paid simultaneously – either from the electronic cash ledger (pre-deposited funds) or by offsetting available credit from the electronic credit ledger.

| GSTR-3B is self-declared. The government does not auto-populate all values for you. You fill in the numbers – and you are responsible for their accuracy. Discrepancies between GSTR-3B and GSTR-1, or between GSTR-3B and GSTR-2B, are flagged automatically by the system and can trigger scrutiny notices. |

What Information is Included in GSTR-3B?

- Total value of outward taxable supplies (your sales for the period)

- Tax collected: IGST, CGST, SGST / UTGST, and applicable cess

- Eligible ITC claimed on inward supplies (purchases)

- ITC reversals: where credit is ineligible or must be returned

- Net tax payable after adjusting all available ITC

- Interest and late fee, if applicable

Who Files GSTR-3B and When?

All regular GST-registered taxpayers must file GSTR-3B. Due dates vary by filing category:

- Monthly filers: 20th of the following month

- Quarterly QRMP filers – Category I states (larger states): 22nd of the month after the quarter

- Quarterly QRMP filers – Category II states (smaller / north-eastern states): 24th of the month after the quarter

Composition scheme dealers are exempt from GSTR-3B. They operate under a separate, simplified return structure.

GSTR-1 vs GSTR-3B: Major Differences

The table below sets out the key distinctions between the two returns in one place:

| Feature | GSTR-1 | GSTR-3B |

|---|---|---|

| Nature | Detailed, invoice-level reporting | High-level summary return |

| What it covers | Outward supplies (sales only) | Sales + ITC claimed + tax payment |

| Auto-populated? | No — filed manually by taxpayer | Partially (draws from GSTR-1 & 2B) |

| Tax payment | No tax payment here | Yes — liability settled on filing |

| Filing frequency | Monthly 11th / Quarterly 13th | Monthly 20th / Quarterly 22nd–24th |

| Impacts buyer’s ITC? | Yes — directly and immediately | No direct impact on buyer |

| Can it be revised? | Yes — via amendment in later period | No — once filed, cannot be revised |

| Nil filing required? | Yes | Yes |

How GSTR-1 and GSTR-3B Work Together

These two returns do not operate in isolation. They are two sides of the same compliance coin, and the government’s system is built to verify them against each other – and against what your suppliers and buyers have reported.

The Monthly Filing Workflow

- Raise invoices and record all sales transactions during the month

- File GSTR-1 by the 11th – uploading all invoice details at the line level

- Your buyer’s GSTR-2B is auto-populated with the invoices you have uploaded

- Reconcile your purchase register against your own GSTR-2B before the 20th

- File GSTR-3B by the 20th – declaring aggregate sales, claiming eligible ITC, and paying net tax

The ITC Rule You Cannot Afford to Ignore

Since 2022, the GST law has significantly tightened ITC claims. A taxpayer can claim ITC in GSTR-3B only up to 105% of the ITC that appears in GSTR-2B. Claiming credit for invoices that do not appear in GSTR-2B – because a supplier has not yet filed their GSTR-1 – can result in demand notices and interest at 18% per annum.

| This rule makes it essential to not only file your own returns on time, but to actively monitor whether your suppliers are filing theirs. A supplier who consistently delays GSTR-1 is costing you real, recoverable money every single month. |

Late Filing Penalties for GSTR-1 and GSTR-3B

Delayed filing is not merely inconvenient – the financial consequences compound quickly:

- Late fee for GSTR-1: ₹50 per day (₹25 CGST + ₹25 SGST) for returns with supplies; ₹20 per day for nil returns

- Late fee for GSTR-3B: Same structure – ₹50 per day for taxable returns, ₹20 per day for NIL

- Interest on unpaid tax: 18% per annum, calculated from the due date of payment

- Cascading effect: GSTR-3B cannot be filed if GSTR-1 for that period is still outstanding

- Buyer impact: Your delayed GSTR-1 blocks your buyer’s ITC – damaging the commercial relationship

- Registration risk: Habitual non-filers face cancellation of GST registration – a consequence now being actively enforced

Conclusion

GSTR-1 and GSTR-3B are not interchangeable returns. One reports invoice-level sales data, while the other handles GST liability and tax payment. Both are mandatory, both are interconnected, and both must be filed accurately and on time.

Businesses that treat GST filing casually often face notices, blocked ITC, vendor disputes, and financial penalties. On the other hand, businesses with a disciplined reconciliation process rarely encounter major compliance issues.

FAQs

Yes, nil GSTR-1 filing is mandatory even if no sales occurred during the tax period.

No, GSTR-3B cannot be revised once submitted. Corrections must be adjusted in future returns.

Buyers may not receive ITC in their GSTR-2B, which can lead to disputes and GST notices.

Both are equally important because one handles invoice reporting while the other handles tax payment.