Skipping your Income Tax Return might feel harmless at first. After all, many people think that if tax is already deducted or income is low, filing is optional.

However, that assumption can quietly create bigger problems.

In reality, not filing your ITR can affect your finances, future plans, and even your credibility. So before you decide to ignore it, let’s break down what actually happens and what you should do next.

Who Needs to File ITR in India?

You generally need to file ITR if:

- Your income exceeds the basic exemption limit

- You want to claim a tax refund

- You have foreign income or assets

- You want to carry forward losses

- You are applying for loans or visas

Even if your tax is already deducted through TDS, filing is still important in many cases.

What Happens If You Don’t File ITR?

Now let’s get into the real impact. These are not just legal points. They affect real-life decisions.

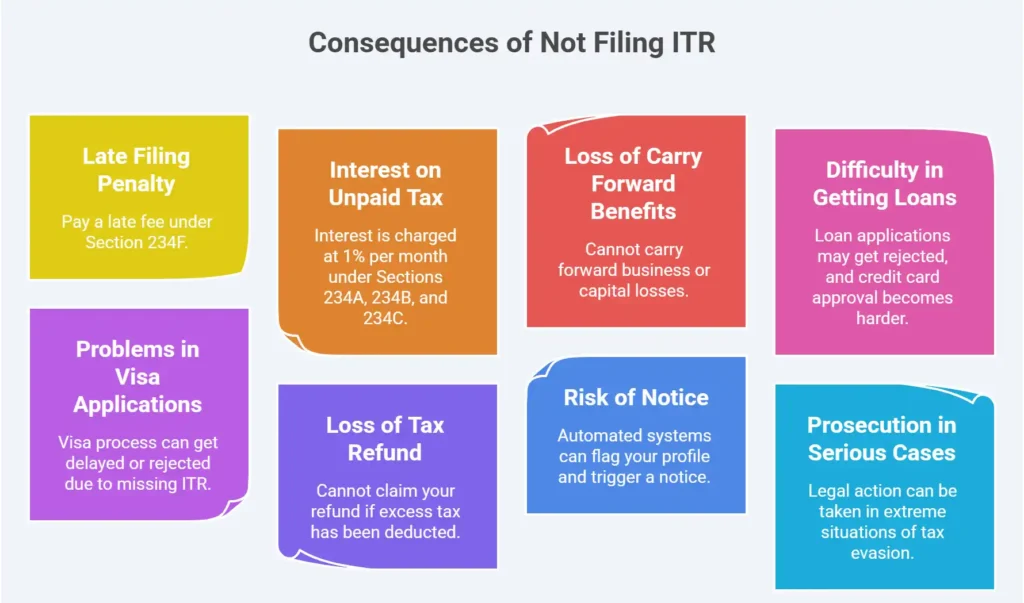

1. Late Filing Penalty

If you miss the deadline, you may have to pay a late fee under Section 234F:

- Up to ₹5,000 if your income is above ₹5 lakh

- Up to ₹1,000 if your income is below ₹5 lakh

So while the amount may look small, it is still an unnecessary cost.

2. Interest on Unpaid Tax

If you have unpaid taxes, interest starts adding up.

Under Sections 234A, 234B, and 234C:

- Interest is charged at 1% per month or part of a month

Over time, this can increase your total tax liability significantly.

3. Loss of Carry Forward Benefits

This is where most people lose money without realizing it.

If you do not file your ITR on time:

- You cannot carry forward business or capital losses

As a result, you miss the chance to reduce future tax liability.

Exception: House property loss can still be carried forward even if filed late.

4. Difficulty in Getting Loans or Credit Cards

Banks and financial institutions often ask for ITR as income proof.

So if you skip filing:

- Your loan application may get rejected

- Credit card approval becomes harder

In simple terms, your financial credibility takes a hit.

5. Problems in Visa Applications

If you plan to travel abroad, this becomes important.

Many embassies require:

- Last 2 to 3 years of ITR

Without it, your visa process can get delayed or rejected.

6. Loss of Tax Refund

If excess tax has been deducted and you don’t file ITR:

- You cannot claim your refund

This means your own money stays stuck with the government.

7. Risk of Notice from Income Tax Department

If your income is visible through:

- TDS

- bank transactions

- investments

But if you still don’t file, automated systems can flag your profile and trigger a notice. Notices are triggered via AIS (Annual Information Statement) and data matching systems.

8. Prosecution in Serious Cases

In extreme situations where tax evasion is involved:

- Legal action can be taken

Under Section 276CC:

- Punishment may include imprisonment and fine

However, this usually applies to willful tax evasion, not simple delay.

Common Myths You Should Ignore

Let’s clear a few misconceptions.

- “No tax means no need to file” → Not always true

- “TDS is deducted, so I’m safe” → Filing is still required in many cases

- “Skipping one year is fine” → It can affect future filings and financial records

What Should You Do If You Missed Filing?

If you have already missed the deadline, don’t panic. You still have options.

1. File a Belated Return

You can file a belated return after the due date by paying a penalty.

2. File an Updated Return

Under updated return provisions:

- You can file within 24 months from the end of the relevant assessment year

However, additional tax may apply. Additional tax = 25% or 50% extra, depending on the delay.

3. Take Professional Help

If things feel confusing, getting expert help can save time, money, and stress.

Platforms like AMpuesto can help with tax filing and compliance.

Final Thoughts

Not filing your ITR is not just about avoiding paperwork. It can affect your loans, travel plans, financial credibility, and even future tax savings. On the other hand, filing your return keeps your financial profile clean and gives you flexibility when you need it most. So instead of delaying it, it’s always better to stay compliant and stress-free.

FAQs

No, it is not mandatory just because you filed once. However, you must file ITR every year if you meet the eligibility criteria for that year.

Yes, but only in serious cases involving willful tax evasion. Simple delay or non-filing usually leads to penalties, not jail.

You may have to pay late fees for each year along with interest on unpaid tax. Also, you may lose benefits like loss carry forward and face higher scrutiny.

You cannot file regular returns for all past years. However, you can file updated returns within 24 months from the end of the relevant assessment year, subject to conditions.