That sinking feeling when a GST Show Cause Notice (SCN) lands in your inbox is real. Still, most notices turn out far less scary once you know which rule the officer is using. In fact, almost every GST demand traces back to three provisions: Section 73, Section 74, and the newer Section 74A.

So before you reply to anything, you must do one thing first. You have to check the financial year. Here is why that single step changes everything.

First, Check the Year: The Split-Timeline Rule

The Finance Act 2024 split GST demand law into two clear lanes. Therefore, the year of the disputed transaction decides which rule the department can use.

- Up to FY 2023-24: Sections 73 and 74 stay fully active. They govern every old audit and back-period dispute.

- From FY 2024-25 onwards: Sections 73 and 74 are gone. Instead, the unified Section 74A handles all fresh demands.

In short, you cannot pick the right defense until you know the year. Now let us break down each track.

Also Read: [Section 122 of CGST Act]

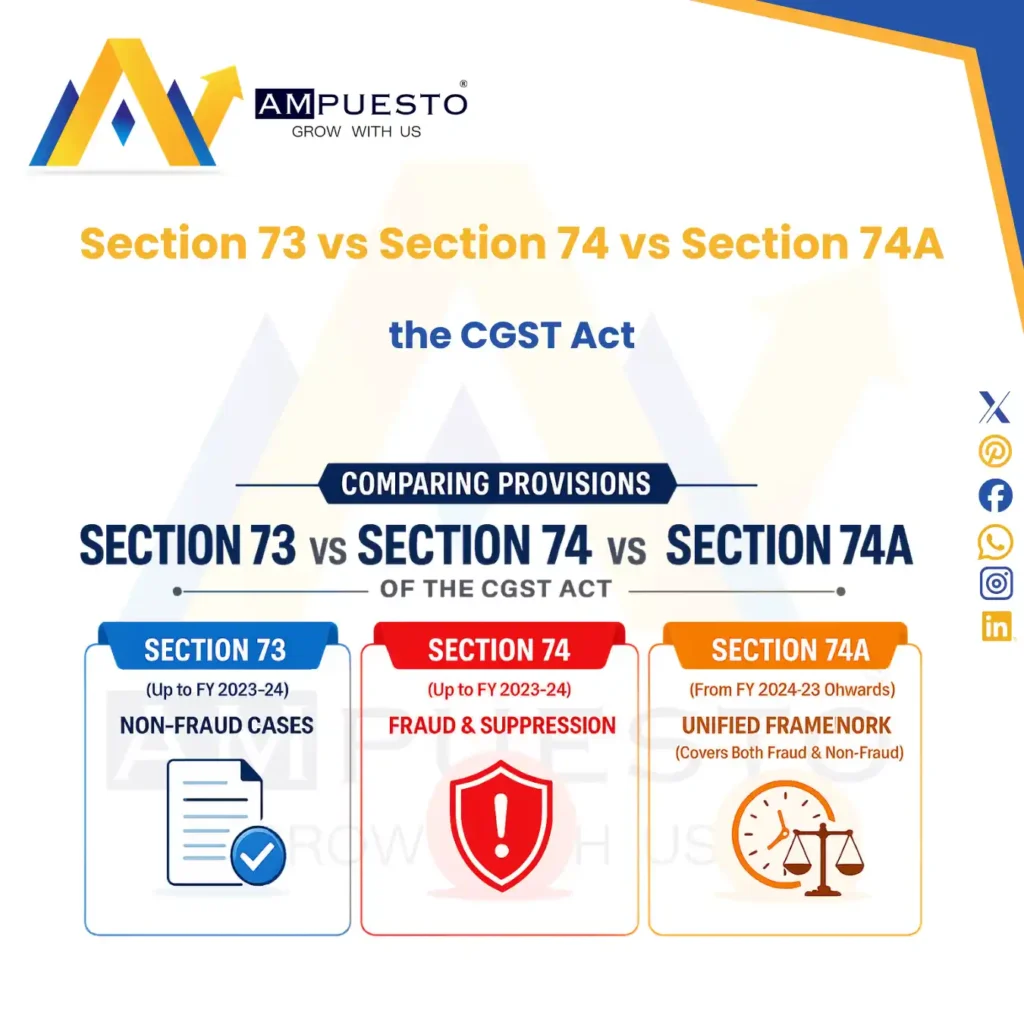

Section 73: The Honest Mistake Track (Up to FY 2023-24)

Section 73 kicks in when you underpay tax, claim a wrong refund, or take incorrect Input Tax Credit (ITC) by genuine error. Crucially, there is no fraud and no intent to evade.

For example, imagine your accountant enters one sales invoice twice in GSTR-1. As a result, your ITC looks inflated. Clearly, that is a clerical slip, not cheating.

Common triggers include:

- A mismatch between GSTR-1 and GSTR-3B figures

- Wrong classification of goods or services that leads to short payment

- A refund claimed because of a simple calculation error

Penalty under Section 73

Thankfully, the penalties stay light here:

- Pay before the SCN: zero penalty

- Pay within 30 days of the SCN: zero penalty

- Pay after the order: 10% of the tax or ₹10,000, whichever is higher

Time limit under Section 73

The officer must pass the final order within 3 years of the GSTR-9 (annual return) due date for that year. Moreover, the SCN has to reach you at least 3 months before that deadline.

Section 74: The Fraud Track (Up to FY 2023-24)

Section 74 is a tougher beast. It applies only when the shortfall links to fraud, willful misstatement, or suppression of facts with intent to evade tax. So the word “intent” sits at the very center of this section.

Typical Section 74 triggers include:

- Claiming ITC on fake or dummy invoices

- Deliberately hiding sales to cut the tax bill

- Collecting GST from customers but never paying it to the government

A key legal shield

However, the department cannot wave the fraud flag casually. The Supreme Court and several High Courts have repeatedly held that Section 74 needs real evidence of fraud. Mere suspicion or an honest interpretation dispute simply does not count.

Penalty under Section 74

Because these cases are serious, the penalties climb fast:

- Pay before the SCN: tax + interest + 15% penalty

- Pay within 30 days of the SCN: tax + interest + 25% penalty

- Pay within 30 days of the order: tax + interest + 50% penalty

- Pay later: tax + interest + 100% penalty (your tax bill effectively doubles)

Time limit under Section 74

Here the department gets a longer leash. It must pass the order within 5 years of the annual return due date, with the SCN reaching you at least 6 months before that.

Section 74A: The New Unified Track (FY 2024-25 Onwards)

For years, officers often invoked Section 74 even for plain mistakes. Why? Because the fraud route handed them the longer 5-year window. To stop that habit, the government introduced Section 74A.

From FY 2024-25, the two separate tracks merge into one. Consequently, here is what changes:

- One time limit for all. The 3-year versus 5-year split is gone. Instead, the officer must issue the SCN within 42 months (about 3.5 years) of the annual return due date, whether fraud is alleged or not. The order then follows within 12 months of the SCN, extendable by another 6 months.

- Small disputes dropped. No notice goes out if the total tax gap for the year stays below ₹1,000.

Penalty and Relief under Section 74A

While Section 74A brings both mistakes and fraud into a single timeline, your penalties still depend strictly on your intent. The major change here is that the government has doubled your breathing room to settle disputes by extending relief windows from 30 days to 60 days.

Here is how the penalty tracks split under the new law:

1. For Non-Fraud Cases (Honest Mistakes):

- Pay before the SCN or within 60 days of its issuance: Zero penalty

- Pay after the order is passed: 10% of the tax amount or ₹10,000, whichever is higher.

2. For Fraud Cases (Intentional Evasion):

- Pay before the SCN is issued: Tax + interest + 15% penalty

- Pay within 60 days of the SCN: Tax + interest + 25% penalty

- Pay within 60 days of the Adjudication Order: Tax + interest + 50% penalty

- Pay later: Tax + interest + 100% penalty (your tax bill doubles).

Quick Comparison: Section 73 vs 74 vs 74A

| Parameter | Section 73 (Legacy) | Section 74 (Legacy) | Section 74A (Modern) |

|---|---|---|---|

| Applicability | Up to FY 2023-24 | Up to FY 2023-24 | FY 2024-25 onwards |

| Grounds | Non-fraud / Mistake | Fraud / Evasion | Unified (Covers both) |

| SCN Window | 3 months before order | 6 months before order | Within 42 months from GSTR-9 due date |

| Order Window | 3 years from GSTR-9 due date | 5 years from GSTR-9 due date | 12 months from SCN (extendable by 6 months) |

| Cure Period | 30 days | 30 days | 60 days |

| Penalty (Paid within Cure Period) | 0% | 25% | 0% (Non-Fraud) 25% (Fraud) |

| Max Penalty | 10% or ₹10,000 | 100% of tax | 10% or ₹10,000 (Non-Fraud) 100% of tax (Fraud) |

Do Not Overlook Section 128A: The One-Time Amnesty

Here is a point many guides skip. Alongside 74A, the Finance Act 2024 also added Section 128A. Basically, it offered a conditional waiver of interest and penalty for Section 73 (non-fraud) demands covering FY 2017-18, 2018-19, and 2019-20.

The catch? Taxpayers had to pay the full principal tax by 31 March 2025. So if you paid on time, you can still claim the waiver order through Rule 164 of the CGST Rules. Sadly, if you missed that date, the waiver is gone, although the regular Section 73 penalty relief may still help.

Got a GST Notice in 2026? Here Is Your Game Plan

First, do not panic. Then work through these steps in order:

1. Check the year first. If an officer tries to issue a legacy Section 73 or Section 74 notice for periods covering FY 2024-25 or later, the notice faces a fundamental jurisdictional flaw. The law mandates that all fresh disputes must be processed under Section 74A. Frame this lack of statutory authority as your primary preliminary objection.

2. Read the allegation. Is it an honest slip or alleged suppression? For a legacy Section 74 notice with no evidence of fraud, attack the “intent” claim to slash the penalty.

3. Use the clock. Pay early, within 30 days for old years or 60 days for new ones, and you can wipe out or sharply cut the penalty.

4. Reconcile, then reply. Pull your GSTR-1, GSTR-3B, and books of accounts. Next, file a clear reply in Form DRC-06 with invoices and ledgers, and always request a personal hearing.

Conclusion

In the end, the shift from Sections 73 and 74 to the unified Section 74A marks a big change for Indian GST. On the bright side, it stops officers from stretching fraud charges just to buy more time. Yet it also widens audit exposure for honest taxpayers, from 36 months to 42 months on newer years. Therefore, your best defense stays simple: keep clean records, reconcile every month, and close gaps before they grow into a notice.

FAQs

1. What is the main difference between Section 73 and Section 74 of the CGST Act?

Intent. Section 73 covers honest mistakes with no fraud, while Section 74 covers fraud, willful misstatement, or suppression with intent to evade tax. As a result, Section 74 carries much heavier penalties.

2. Does Section 74A replace Sections 73 and 74?

Yes, but only from FY 2024-25 onwards. For FY 2017-18 through FY 2023-24, Sections 73 and 74 still apply fully.

3. What is the time limit to issue a GST demand notice?

Under Section 73 it is 3 years from the GSTR-9 due date, under Section 74 it is 5 years, and under Section 74A it is 42 months for every case.

4. Can a Section 74 case be reclassified as Section 73?

Yes. If the department cannot prove fraud or intent, courts and appellate authorities can shift the demand to Section 73, which then lowers the penalty.