If you are a seller or collector responsible for Collecting Tax Collected at Source (TCS) in India, Form 27EQ is a document you simply cannot ignore. Yet many businesses and tax professionals find themselves confused about what it means, when to file it, and exactly how the process works. This guide breaks it all down – clearly, accurately, and step by step.

What Is Form 27EQ?

Form 27EQ is a quarterly return for Tax Collected at Source (TCS) that must be filed by every person responsible for collecting TCS with the Income Tax Department of India.

Unlike TDS, where tax is deducted before making a payment, TCS is collected by the seller from the buyer at the time of sale of specified goods or services. Form 27EQ serves as a consolidated statement of all TCS transactions recorded during a particular quarter.

It is governed by Section 206C of the Income Tax Act, 1961, and filed in accordance with Rule 31AA of the Income Tax Rules.

Who Should File Form 27EQ?

Any person or entity responsible for collecting Tax Collected at Source (TCS) is required to file Form 27EQ. This applies to sellers who collect TCS on the sale of specified goods or services, including:

- Alcoholic liquor for human consumption

- Timber, tendu leaves, and other forest produce

- Scrap

- Minerals such as coal, lignite, and iron ore

- Motor vehicles priced above ₹10 lakh

- Parking lots, toll plazas, and mining or quarrying rights

- Foreign remittances and overseas tour packages

- Sale of goods exceeding ₹50 lakh in a financial year under Section 206C(1H)

Whether you are an individual seller, a company, a partnership firm, or a government entity, if you collect TCS, filing Form 27EQ is mandatory.

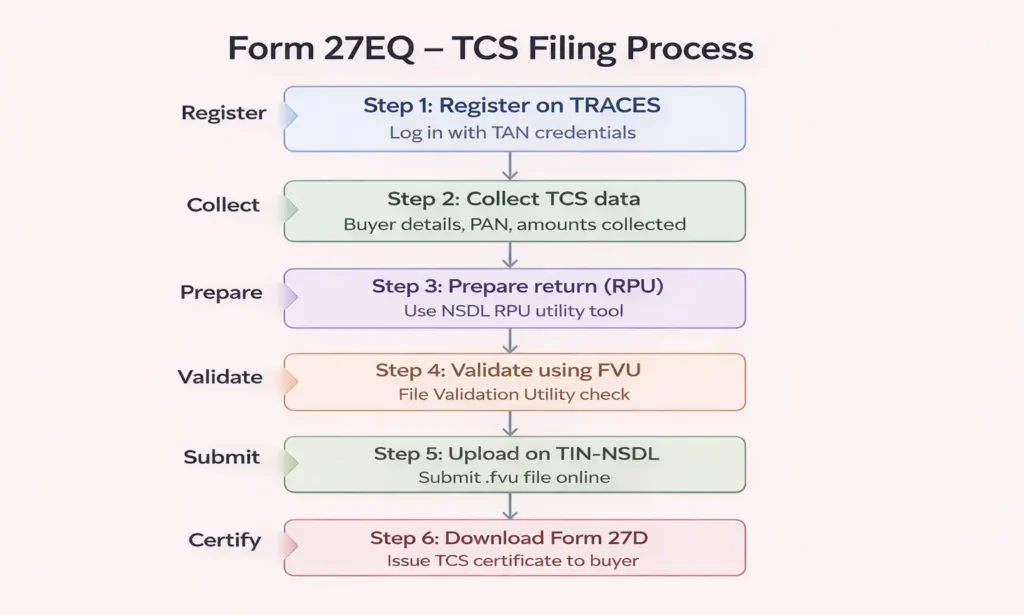

Form 27EQ Filing Process

Filing Form 27EQ is a structured process that ensures accurate reporting of Tax Collected at Source (TCS). If you follow each step carefully, the filing becomes straightforward and error-free. Here is how the complete process works:

Step 1: Register on TRACES

Start by logging into the TRACES portal using your TAN credentials. If you are not registered, complete the registration first. This platform is where all TCS-related activities are managed, so access to it is essential.

Step 2: Collect TCS Data

Next, gather all the required data. This includes buyer details, PAN information, and the total amount on which TCS has been collected. Accuracy matters here because even small errors can lead to rejection later.

Step 3: Prepare the Return (RPU)

Use the Return Preparation Utility (RPU) provided by NSDL to prepare your TCS return. This tool helps you structure the data correctly in the prescribed format. Make sure all entries are validated before moving forward.

Step 4: Validate Using FVU

Once the return is prepared, validate the file using the File Validation Utility (FVU). This step checks for errors or inconsistencies. If any issues are found, correct them in the RPU and validate again.

Step 5: Upload to TIN-NSDL

After successful validation, upload the .fvu file to the TIN-NSDL portal. This is the actual submission step where your return is officially filed with the system.

Step 6: Download Form 27D

Finally, once the return is processed, download Form 27D from TRACES. This is the TCS certificate that needs to be issued to the buyer as proof of tax collection.

Key Details Mentioned in Form 27EQ

Form 27EQ isn’t just a summary; it’s a detailed statement that captures-

- Seller/ Collector information: Name, TAN(tax Deduction and Collection Account Number), PAN, and address

- Buyer information: Name, PAN, and type of buyer( government/non-government)

- Nature of goods and services on which TCS is applicable

- Amount collected and the TCS rate applied

- Date of collection and date of remittance to the government

- Challan details through which TCS was deposited

- PAN/Aadhaar status: Whether the buyer has furnished a valid PAN or Aadhaar, details need to undergo cross-verification, which is easy for both the taxpayer and the Income Tax Department.

Form 27EQ Due Dates

| Quarter | Period | Due Date for Form 27EQ |

|---|---|---|

| Q1 | April 1 – Jun 30 | July 15 |

| Q2 | July 1 – Sep 30 | October 15 |

| Q3 | Oct 1 – Dec 31 | January 15 |

| Q4 | Jan 1 – Mar 31 | May 15 |

Note: The government may extend the due dates in specific cases. Always check the latest CBDT notifications or circulars for any variations.

TCS Deposit Due Dates

Before filing Form 27EQ, you must first deposit the collected TCS with the government. Timely payment is essential to avoid penalties and ensure smooth return filing.

The due dates for depositing TCS are as follows:

- For April to February: TCS must be deposited by the 7th of the following month

- For March: TCS must be deposited by April 30

Late Filing Fees & Penalties for Form 27EQ (Section 234E & 271H Explained)

Delay in filing Form 27EQ can lead to financial penalties and compliance issues. Here is what you need to know:

- Late filing fee under Section 234E: ₹200 per day is charged until the return is filed, subject to a maximum of the total TCS amount

- Penalty under Section 271H: A minimum penalty of ₹10,000, which can go up to ₹1,00,000 for non-filing or incorrect filing of the return

- Disallowance of expenses: If TCS is not deposited correctly, related expenses may be disallowed while calculating business income

To stay compliant, ensure that TCS is deposited and Form 27EQ is filed within the prescribed due dates. Setting reminders or maintaining a compliance calendar can help you avoid unnecessary penalties.

Form 27EQ vs Form 27D: Key Differences Explained

Many taxpayers confuse Form 27EQ with Form 27D. While both are related to TCS, they serve completely different purposes. Here is a simple comparison to help you understand the difference clearly:

| Feature | Form 27EQ | Form 27D |

|---|---|---|

| Nature | Quarterly TCS return filed by the seller or collector | TCS certificate issued to the buyer |

| Filed with / Issued by | Submitted to the Income Tax Department through TIN-NSDL | Issued to the buyer after return processing via TRACES |

| Who files/generates | Filed by the seller or collector | Generated from TRACES by the seller and issued to the buyer |

| Purpose | Reporting TCS collected during a quarter | Serves as proof of TCS for the buyer to claim the tax credit |

Common Form 27EQ Filing Mistakes and How to Avoid Them

Even experienced filers can make mistakes while filing Form 27EQ, which may lead to notices, penalties, or rejection of returns. Here are some common errors you should avoid:

- Incorrect PAN of the buyer: If the buyer’s PAN is missing or incorrect, TCS may be charged at a higher rate, and the buyer may not be able to claim tax credit

- Wrong challan mapping: Each TCS entry must be correctly linked to the respective challan used for deposit. Incorrect mapping can cause mismatches during verification

- Using outdated RPU or FVU versions: Always use the latest utilities for return preparation and validation, as older versions may fail current checks

- Not issuing Form 27D: Filing Form 27EQ is only part of the process. Issuing the TCS certificate to the buyer is equally important

- Filing nil returns unnecessarily: If there are no TCS transactions in a quarter, filing a nil return is usually not required. However, always verify the latest guidelines before skipping filing

Conclusion: Why Accurate Form 27EQ Filing Matters

Form 27EQ plays a key role in India’s tax compliance system by ensuring proper reporting of TCS on specified goods and services. For sellers and collectors, timely and accurate filing is not just a legal requirement but also builds trust with buyers who depend on Form 27D to claim their tax credit.

What this really means is simple. When your filings are accurate and on time, you avoid penalties, reduce compliance risks, and maintain credibility with both the tax authorities and your customers.

FAQs

1. What is Form 27EQ used for?

Form 27EQ is used to report Tax Collected at Source (TCS) on specified goods and services. It is a quarterly return filed by sellers or collectors with the Income Tax Department.

2. Is it mandatory to file Form 27EQ?

Yes, filing Form 27EQ is mandatory for any person or entity that collects TCS. Failure to file can result in late fees and penalties under Sections 234E and 271H.

3. What is the difference between 27Q and 27EQ?

Form 27Q is a TDS return filed for payments made to non-residents, while Form 27EQ is a TCS return filed for tax collected on the sale of specified goods and services. In simple terms, 27Q deals with tax deducted, whereas 27EQ deals with tax collected.

4. How to generate a TDS certificate for 27EQ?

For Form 27EQ, the relevant certificate is Form 27D, not a TDS certificate. You can generate Form 27D from the TRACES portal after filing and processing the return.